Whether you are new to homeschooling or you have been homeschooling for a while with students moving up to another level, this article will provide guidelines to consider when making plans for your students.

Although the suggestions I make in this article are general and eclectic, it may be worth your while to take a look at the multiple styles and methods of homeschooling. You may be surprised at the many choices and philosophies available for your consideration. There is no right or wrong choice. You may try out one style only to discover it is not the best fit for your family. In the end, you may find the best plan is to pick and choose from various styles in order to design a plan that works for you and your family. Two books that will encourage you in your homeschooling journey are Teaching from Rest: A Homeschooler’s Guide to Unshakable Peace by Sarah McKenzie and Mere Motherhood by Cindy Rollins.

ELEMENTARY SCHOOL

For elementary students, keep it simple and keep it fun. Creating a love of learning is the key to raising students who are academically successful. Do not worry about curriculum. It is available for your use, but you have done well teaching your children from birth to age 5 without curriculum, so if you want to continue in the same manner,  go for it! The freedom and flexibility of homeschooling allows you to plan your students’ experiences around their learning style and their interests. If you do purchase a curriculum and it is not working the way you envisioned, feel free to set it aside, sell it, or give it away. Do not become enslaved to curriculum. If you feel a need to make purchases then purchase Legos, critical thinking games, a globe and maps, and fun items that inspire the imagination. During the younger years, a huge emphasis should be placed on reading aloud, enjoying nature, having discussions, and playing games. Go on fieldtrips. Visit museums, science centers, and zoos. Oftentimes, the cost of an annual family membership is not much more than the cost of a one-day visit, and many zoos and museums have reciprocal memberships! Involve your children in meal planning and grocery shopping. Reach out to your community and volunteer for opportunities to serve that allow your children to participate. Encourage your students to ask questions, and then guide them towards learning how to find the answers to their questions. No one can know everything, but students who learn how to find the answers to their questions become independent learners, allowing parents the luxury of not worrying about whether their students will succeed academically, or be left behind. Look for an upcoming article with specifics on how to encourage inquisitiveness and how to teach your students to find answers from reliable resources! When you have a few minutes, listen to Sir Ken Robinson’s Ted Talk on How Schools Kill Creativity.

go for it! The freedom and flexibility of homeschooling allows you to plan your students’ experiences around their learning style and their interests. If you do purchase a curriculum and it is not working the way you envisioned, feel free to set it aside, sell it, or give it away. Do not become enslaved to curriculum. If you feel a need to make purchases then purchase Legos, critical thinking games, a globe and maps, and fun items that inspire the imagination. During the younger years, a huge emphasis should be placed on reading aloud, enjoying nature, having discussions, and playing games. Go on fieldtrips. Visit museums, science centers, and zoos. Oftentimes, the cost of an annual family membership is not much more than the cost of a one-day visit, and many zoos and museums have reciprocal memberships! Involve your children in meal planning and grocery shopping. Reach out to your community and volunteer for opportunities to serve that allow your children to participate. Encourage your students to ask questions, and then guide them towards learning how to find the answers to their questions. No one can know everything, but students who learn how to find the answers to their questions become independent learners, allowing parents the luxury of not worrying about whether their students will succeed academically, or be left behind. Look for an upcoming article with specifics on how to encourage inquisitiveness and how to teach your students to find answers from reliable resources! When you have a few minutes, listen to Sir Ken Robinson’s Ted Talk on How Schools Kill Creativity.

MIDDLE SCHOOL

Although planning for middle school is not quite as important as the high school years, parents should begin getting serious about their students’ academic studies. During the elementary years you have, hopefully, instilled in your children a love of learning as well as having equipped them with the ability to find answers to their questions. The middle school years are challenging because of the physiological changes that start taking place and those changes often result in undesired attitudes surfacing. Expediting an academic plan may be fraught with the need to address character issues. Be sure you address the character issues. If you need to set aside academics in order to restore relationships or repair damage done by students who are acting out, do so. Do not be afraid to have non-negotiable parental mandates, but explain to your students the reasoning behind the decisions and  directions you pursue. They do not have to understand or agree with your decisions, but your students should be required to respond respectfully to you (and to others).

directions you pursue. They do not have to understand or agree with your decisions, but your students should be required to respond respectfully to you (and to others).

In addition to teaching your students how to answer questions, middle school is a great time to encourage students to question answers, but to do so respectfully. (Are you seeing a correlation to middle school and character issues?) If you have already lived through the middle school years you may chuckle at the advice to encourage your students to question answers because that tends to be natural for middle school students. They tend to question everything, particularly rules and expectations set forth by parents. Avoid answering with, “Because I said so,” if possible. You will gain respect if you take the time to share your heart and, even if your students are not mature enough to understand or agree with your explanation, they are apt to be less frustrated than they would be otherwise. Now that character issues have been addressed, let’s talk about subjects to cover.

Math: During middle school make sure your students have a firm understanding of basic math facts so that they will be adequately prepared to be introduced to algebra and geometry in high school. Being able to multiple mentally, whether by memorizing the times table or using another method to achieve that result, is imperative. Knowing how to divide without using a calculator is also important. Understanding percentages and fractions is equally important to having a firm foundation for higher level math classes.

English: In high school your student should begin writing essays so while in middle school introduce your students to simple writing assignments such as book reports, short stories, testimonies, and more. Continue to read aloud, but assign great literature to be read by your students as well. You may find your students are willing to read more if they are allowed to read the biographies found in the juvenile section of the library. Rather than reading one biography that is over 200-300 pages long, your student can read five or six, or more, biographies that are of much shorter length. There are many resources for literature-driven curriculum.

History: I was that student who thought history was the most boring subject on the planet until I began homeschooling my students and discovered historical fiction! Reading books that brought history to life led me to have a deep love for history! Introduce your students to history through literature or through unit studies! For American history, the House of Winslow series is very historically accurate. If your students are reading biographies, then chances are they may want to further pursue information about the period of history being covered by the biography they are reading. With one of my sons (who loves history), we went through the Timetables of History (a chronological record of history from the beginning of written records) and when something sparked further interest, we looked up videos and articles pertaining to that event. For those looking for a literature-based history curriculum, TruthQuest may be just what you need.

Science: Because your student will be taking biology and chemistry in high school, the middle school years should include an introduction to basic science that includes life, earth, and physical science. If you are going for a more literature based approach, include biographies of great scientists. One of my favorite books to read aloud is Carry On Mr. Bowditch. Books about George Washington Carver were enjoyed as well. As far as text books go, many families choose to use Apologias books for science.

Electives: In addition to the basics, you may choose to add in any number of electives from physical education to music, foreign language, leadership, religions and worldviews, shop, cooking, or anything else that particularly interests your students.

HIGH SCHOOL

Now is definitely the time to make specific plans for your students. Although you will have some flexibility, in order to ensure that your students are adequately prepared for life after high school, it is important to plan ahead. Be sure you prepare your students for college, whether they think they need college, or not. It is better to be prepared and not need it, than vice versa. I wrote an blog post that will help you avoid eight common mistakes that homeschooling parents make. If your students have no idea what they want to pursue after high school, help them discover their gifts, talents, and passions. Narrow down top college choices so you can find out what is expected from those colleges as far as admission requirements, transcript expectations, and scholarship potential. Feel free to download The Journey, a free e-resource that will help you plan ahead.

Transcripts: Although most states have suggested guidelines for high school graduation, there are no set-in-stone laws, so you have the freedom to plan according to what’s best for your student. The expectation is that a four-year high school transcript will include 22 to 24 credits. Most states expect a student to take at least 3 math classes, 3 or 4 English classes, 3 science classes (with at least 2 labs), 3 social studies, ½ credit for personal finance, 1 or 2 physical education credits, 2 foreign language credits, and the remainder as electives. Some states are more rigorous while others are more flexible but, again, these are guidelines and not mandates. Be aware that as flexible as you are allowed to be from a homeschooling point-of-view, you may find particular colleges have requirements that your student must fulfill in order to attend that college. For this reason, narrowing down college choices is vital to planning the courses for your students. Some homeschooling families have their students take a 5th year of high school and, believe it or not, colleges will accept a 5 year transcript from homeschooled students.

Curriculum: When I began homeschooling (in the 1980s) our curriculum choices were very limited. That is not the case today. There are online programs that are totally free (Easy Peasy and Kahn Academy are two programs often recommended) and there are many programs that can be purchased. There are textbooks available for every subject imaginable and there are products galore for the students who prefer learning without textbooks whether that is with CDs, videos, or with real books.

Course Selection: It is presumed that your student will take English, math, science, and social studies. Most state guidelines suggest two years of the same foreign language, although there are colleges that do not have that requirement. If you know what major your student will pursue, you can better plan which courses to choose. For instance, students who plan to become engineers should take as many math and science classes as possible while in high school. If your students show a particular interest in a subject, then have them take classes pertaining to that subject in order to confirm or refute that interest. If your students have no idea what they want to do after high school, then provide a well-rounded high school experience while trying to nail down a plan for after high school. My next article will include suggestions for helping your children discover their gifts, interests, and passions.

Beyond the Basics: Although we have all been conditioned to believe that including the classes mentioned above are sufficient for a proper education, I would like to suggest that there are classes worth considering that are equally (if not more) important to a well rounded education. Taking classes in current events, speech and debate, apologetics, logic, entrepreneurship and personal finance are classes that will help prepare your students for life after high school whether that includes college, or not. One of my regrets is not having my students involved in debate clubs until the 5th child (of 9) was in high school. Once I became aware of the skills gained being involved in a debate club (there are at least three Christian homeschool debate leagues), my students were required to participate in a debate club for at least one year.

Books: To help plan for the high school years read Celebrate Highschool: Finish with Excellence and More Than Credits: Skills Highschoolers Need for Life both written by Cheryl Bastain.

Test Prep. Because COVID has disrupted the ability for colleges to require test scores for admission and scholarships, many colleges are now test-optional. Whether these colleges will remain test-optional is yet to be known. Before COVID, the highest scholarships were awarded to students with high test scores (ACT, SAT and/or CLT). For that reason, spending time and money on your students so that they could adequately prepare for these tests and, taking the tests multiple times in order to raise their scores, was essential to families needing scholarships for their students (and, to be honest, most of us need all the financial help we can get). At this time, GPAs are being used by test-optional colleges when test scores are not available. For that reason, your students should be encouraged to achieve high grades even if that means repeating classes with poor grades.

Dual Enrollment. Taking college-level classes is a win/win for students who are ready and able to pass college-level classes. Not only will your students receive both high school and college credit, but one college class is usually counted as a full high school credit, meaning your students will earn a year’s worth of high school credit in one semester. This will either allow your student to graduate early or to continue taking college classes during high school. Dual enrollment is free in several states, discounted in some states and, oftentimes, discounted by the college. Bryan College offers dual enrollment classes on line four times a year with a $200 scholarship for out-of-state students and, for Tennessee students, the same scholarship is offered once the state DE grant is used. In fact, a Tennessee student can take 30 credit hours with Bryan College for as little as $600 if the student uses the DE grant, the school scholarship and the HOPE. As wonderful as the dual enrollment opportunity is for high school students, it is not without dangers.

As you make plans for your students’ academic future, take comfort in knowing that you have both the freedom and the flexibility to make adjustments as needed in order to improve your students’ homeschooling experience. There is no black-and-white, or right-or-wrong way to do this. Plan, pray, talk to friends, and research options and everything will eventually come together!

In sharing my personal experience with you, you may be surprised at the lessons I learned through this course. It is certainly different than the advice I had received from several Christian money management programs.

In sharing my personal experience with you, you may be surprised at the lessons I learned through this course. It is certainly different than the advice I had received from several Christian money management programs. Let’s talk about credit cards. Some money management programs suggest one should never get a credit card and that cash only should be used. Currently, that is turning out to be a problem since the pandemic has created situations where cash is not accepted for certain purchases. Credit cards are not, in and of themselves, an evil thing. Credit cards are a tool that many use for convenience, in order to earn points or get cash back, have purchases insured, or to simplify bookkeeping. When credit cards are procured without annual fees and paid off monthly, they offer many advantages to the card holder. Wisely using credit cards builds credit scores and having a credit card enables the card holder to be able to rent cars. One of my daughters uses a particular credit card to earn a free vacation annually. Another daughter was glad her husband used a credit card to rent a car when in Ireland because, when they had a flat tire, the repair was covered by the card. Even though credit cards can be beneficial to those who use them wisely, not everyone should have a credit card. Many people, especially teens, do not handle credit cards wisely and they end up owing more than they can afford (putting them in debt), and the late fees and interest charged for non-payment rack up. Is there a danger in having credit cards? Yes! Just like there is danger in driving a car. One does not get behind the wheel of a car (hopefully) until licensed, insured and prepared to drive. Credit cards in the hands of an irresponsible person is a recipe for disaster.

Let’s talk about credit cards. Some money management programs suggest one should never get a credit card and that cash only should be used. Currently, that is turning out to be a problem since the pandemic has created situations where cash is not accepted for certain purchases. Credit cards are not, in and of themselves, an evil thing. Credit cards are a tool that many use for convenience, in order to earn points or get cash back, have purchases insured, or to simplify bookkeeping. When credit cards are procured without annual fees and paid off monthly, they offer many advantages to the card holder. Wisely using credit cards builds credit scores and having a credit card enables the card holder to be able to rent cars. One of my daughters uses a particular credit card to earn a free vacation annually. Another daughter was glad her husband used a credit card to rent a car when in Ireland because, when they had a flat tire, the repair was covered by the card. Even though credit cards can be beneficial to those who use them wisely, not everyone should have a credit card. Many people, especially teens, do not handle credit cards wisely and they end up owing more than they can afford (putting them in debt), and the late fees and interest charged for non-payment rack up. Is there a danger in having credit cards? Yes! Just like there is danger in driving a car. One does not get behind the wheel of a car (hopefully) until licensed, insured and prepared to drive. Credit cards in the hands of an irresponsible person is a recipe for disaster.  Enrolling your students in this introduction to personal finance is a great first step in making sure they are ready for independent living. If your student takes the class as a dual enrollment class then they will be in an online class with other students. If you purchase the homeschool version, great care has been taken to provide everything you need to easily and successfully deliver the course material. From interactive lessons and resources which will challenge students, to the tutorials and coaching designed to assist instructors, all of the hard work has been done for you. The course practically teaches itself, and you’ll surely find that your students won’t be the only ones learning!

Enrolling your students in this introduction to personal finance is a great first step in making sure they are ready for independent living. If your student takes the class as a dual enrollment class then they will be in an online class with other students. If you purchase the homeschool version, great care has been taken to provide everything you need to easily and successfully deliver the course material. From interactive lessons and resources which will challenge students, to the tutorials and coaching designed to assist instructors, all of the hard work has been done for you. The course practically teaches itself, and you’ll surely find that your students won’t be the only ones learning! Students who have completed the 10th grade with a 3.0 GPA can take this class online with Bryan College, for college credit. If you live outside of Tennessee, a $200 scholarship is available, making the three hour class only $300. For Tennessee students, the DE grant will pay for the class if it’s one of the first two classes taken by the student. After the DE grant is used, a $200 scholarship will be offered to Tennessee students as well. The cost of materials is only $75. If you would like to have your student

Students who have completed the 10th grade with a 3.0 GPA can take this class online with Bryan College, for college credit. If you live outside of Tennessee, a $200 scholarship is available, making the three hour class only $300. For Tennessee students, the DE grant will pay for the class if it’s one of the first two classes taken by the student. After the DE grant is used, a $200 scholarship will be offered to Tennessee students as well. The cost of materials is only $75. If you would like to have your student

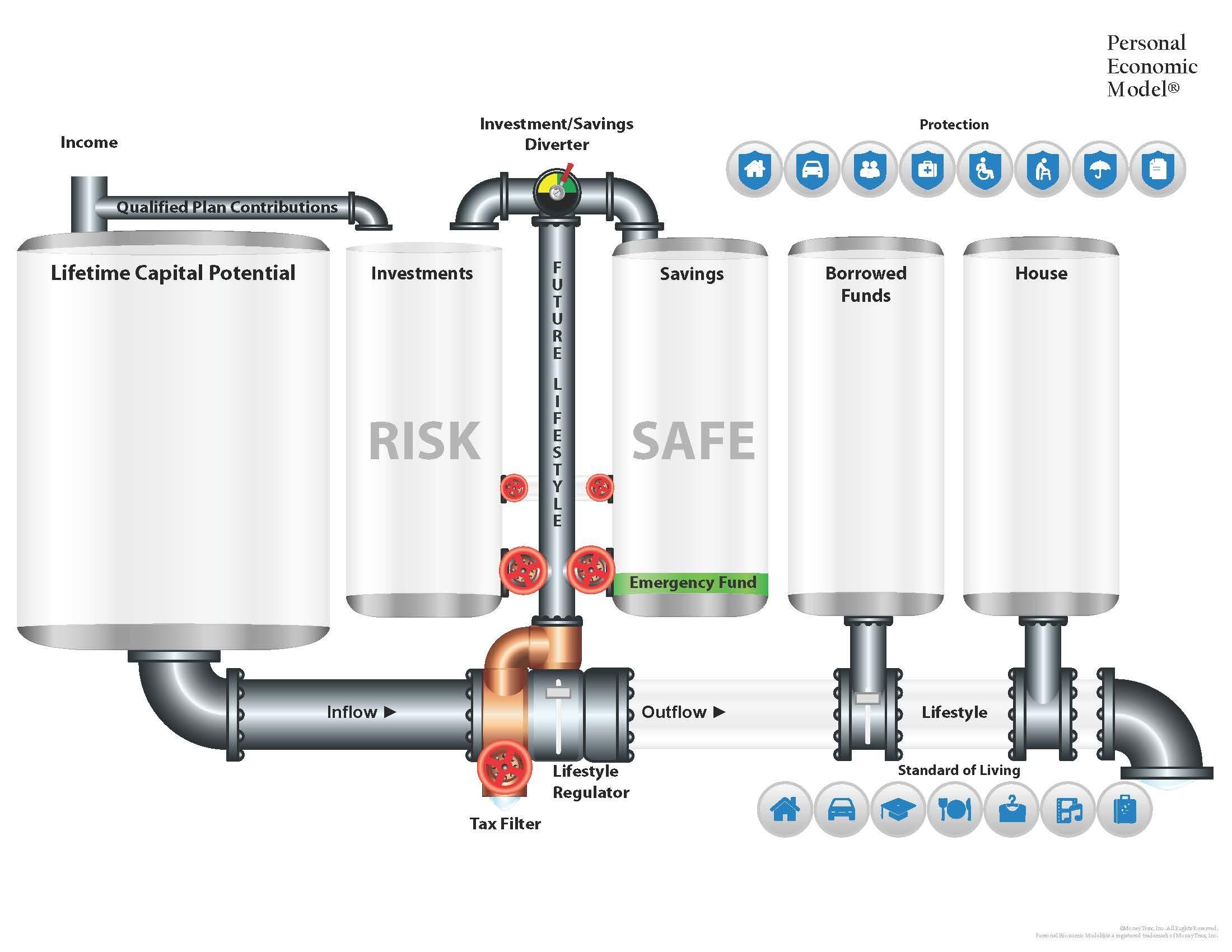

Don Blanton, co-author of the book Personal Economic Model, has designed a three hour college course that will help students understand everything they need to know about the financial world. Using visuals that are interactive, this course takes you from questioning, “Why work?” to helping your student plan wisely to lead a productive and responsible life from high school graduation to retirement (and past retirement age for those who do not choose to retire).

Don Blanton, co-author of the book Personal Economic Model, has designed a three hour college course that will help students understand everything they need to know about the financial world. Using visuals that are interactive, this course takes you from questioning, “Why work?” to helping your student plan wisely to lead a productive and responsible life from high school graduation to retirement (and past retirement age for those who do not choose to retire).