If what you believe about money isn’t true, when would you want to know? I first heard that question from Don Blanton, the founder of PEM life. Most of us would want to know right away if a belief we held was not, in fact, true. Many of us have been taught a thing or two about money that may not be true!

Mr. Blanton has worked to educate more than 20,000 financial advisors in his nearly 30 year career as president and founder of MoneyTrax Inc., and still maintains a successful personal practice as a financial advisor today. The core concepts, tools, and principles which he has developed to teach and train financial services professionals are now being made available through PEM LIFE curricula in an effort to extend financial literacy. Many families spend quite a bit of time and money on their students’ education yet many students graduate with little to no understanding of how to manage the money they will earn.

It is amazing that society puts so much emphasis on reading, writing and arithmetic, but excludes a need for practical lessons on personal finance. This class, available as a three hour dual enrollment class with Bryan College, or as a stand alone class without college credit, is now available to homeschooling families. This class is life-changing.

In sharing my personal experience with you, you may be surprised at the lessons I learned through this course. It is certainly different than the advice I had received from several Christian money management programs.

In sharing my personal experience with you, you may be surprised at the lessons I learned through this course. It is certainly different than the advice I had received from several Christian money management programs.

So, what is it that we have we been taught to believe that may not be true? Most of us have been led to believe that taking out loans should be avoided and that we should pay cash for everything when possible. We have been taught that we should pay off our loans, including mortgages, as soon as possible. We have been taught that having and using credit cards should be avoided. That’s the advice we have heard for many years. My husband and I were introduced to Don Blanton and the PEM class via my son (who was taking the class at Bryan College) right before we were to close on one house and purchase another. My son encouraged me to read the chapter on mortgages and my mind was blown. Mr. Blanton suggests that it might be preferable to take out a 30 year mortgage with a lower down payment rather than using cash on hand for the purchase. What? Don’t invest all the money from one home to another? Don’t go for the lowest loan amount possible? Don’t try and pay off the mortgage sooner rather than later? After reading the chapter I was almost convinced, but not quite — so I called Mr. Blanton and, after asking me a few questions about our situation, he convinced us that it would be wiser to have a higher mortgage amount at a low interest rate so that we would have access to cash for investment, emergencies, ministries, etc. Of course this decision was based on our ability to handle the mortgage payments. That was a year ago. We heeded his advice and have no regrets. We are currently refinancing at a lower interest rate and our monthly payments will be reduced by over $100 each month. We will leave the table with more cash. Do not interpret this as a condemnation on those who choose not to take out loans. Everyone needs to decide what is best in light of their finances and the options available.

We have been led to believe that if we take out a loan, then we are in debt. That is not necessarily true. Debt, as defined by Don Blanton, is when you have an obligation to pay with money that is yet to be earned. That is debt. Taking out a loan does not put you in debt unless you borrow more than you have. You may finance a new car at a low interest rate even though you have enough cash to be able to buy it outright. In that case you have a loan, but you are not in debt. Make sense? You are not having to make payments with future earnings.

Debt is an obligation to pay with money that is yet to be earned. It may take a little time to wrap your head around that. It did for me. When talking to Mr. Blanton about my hesitation to finance any purchase, he pointed out that we finance many expenses, not just those that require a loan. We pay monthly for our electric, wifi, gas, phone, and similar products and services. Those expenses are financed. We do not ask to pay up front in order to avoid a monthly payment, do we? Another lesson your student will learn in this class is that there are always additional costs associated with material possessions. A house is never truly ‘paid off’ because you will always have upkeep, insurance bills, and taxes to pay. Even when a car is purchased for cash or paid off, there are always additional transportation costs including upkeep, repairs, insurance and more.

Let’s talk about credit cards. Some money management programs suggest one should never get a credit card and that cash only should be used. Currently, that is turning out to be a problem since the pandemic has created situations where cash is not accepted for certain purchases. Credit cards are not, in and of themselves, an evil thing. Credit cards are a tool that many use for convenience, in order to earn points or get cash back, have purchases insured, or to simplify bookkeeping. When credit cards are procured without annual fees and paid off monthly, they offer many advantages to the card holder. Wisely using credit cards builds credit scores and having a credit card enables the card holder to be able to rent cars. One of my daughters uses a particular credit card to earn a free vacation annually. Another daughter was glad her husband used a credit card to rent a car when in Ireland because, when they had a flat tire, the repair was covered by the card. Even though credit cards can be beneficial to those who use them wisely, not everyone should have a credit card. Many people, especially teens, do not handle credit cards wisely and they end up owing more than they can afford (putting them in debt), and the late fees and interest charged for non-payment rack up. Is there a danger in having credit cards? Yes! Just like there is danger in driving a car. One does not get behind the wheel of a car (hopefully) until licensed, insured and prepared to drive. Credit cards in the hands of an irresponsible person is a recipe for disaster.

Let’s talk about credit cards. Some money management programs suggest one should never get a credit card and that cash only should be used. Currently, that is turning out to be a problem since the pandemic has created situations where cash is not accepted for certain purchases. Credit cards are not, in and of themselves, an evil thing. Credit cards are a tool that many use for convenience, in order to earn points or get cash back, have purchases insured, or to simplify bookkeeping. When credit cards are procured without annual fees and paid off monthly, they offer many advantages to the card holder. Wisely using credit cards builds credit scores and having a credit card enables the card holder to be able to rent cars. One of my daughters uses a particular credit card to earn a free vacation annually. Another daughter was glad her husband used a credit card to rent a car when in Ireland because, when they had a flat tire, the repair was covered by the card. Even though credit cards can be beneficial to those who use them wisely, not everyone should have a credit card. Many people, especially teens, do not handle credit cards wisely and they end up owing more than they can afford (putting them in debt), and the late fees and interest charged for non-payment rack up. Is there a danger in having credit cards? Yes! Just like there is danger in driving a car. One does not get behind the wheel of a car (hopefully) until licensed, insured and prepared to drive. Credit cards in the hands of an irresponsible person is a recipe for disaster.

Enrolling your students in this introduction to personal finance is a great first step in making sure they are ready for independent living. If your student takes the class as a dual enrollment class then they will be in an online class with other students. If you purchase the homeschool version, great care has been taken to provide everything you need to easily and successfully deliver the course material. From interactive lessons and resources which will challenge students, to the tutorials and coaching designed to assist instructors, all of the hard work has been done for you. The course practically teaches itself, and you’ll surely find that your students won’t be the only ones learning!

Enrolling your students in this introduction to personal finance is a great first step in making sure they are ready for independent living. If your student takes the class as a dual enrollment class then they will be in an online class with other students. If you purchase the homeschool version, great care has been taken to provide everything you need to easily and successfully deliver the course material. From interactive lessons and resources which will challenge students, to the tutorials and coaching designed to assist instructors, all of the hard work has been done for you. The course practically teaches itself, and you’ll surely find that your students won’t be the only ones learning!

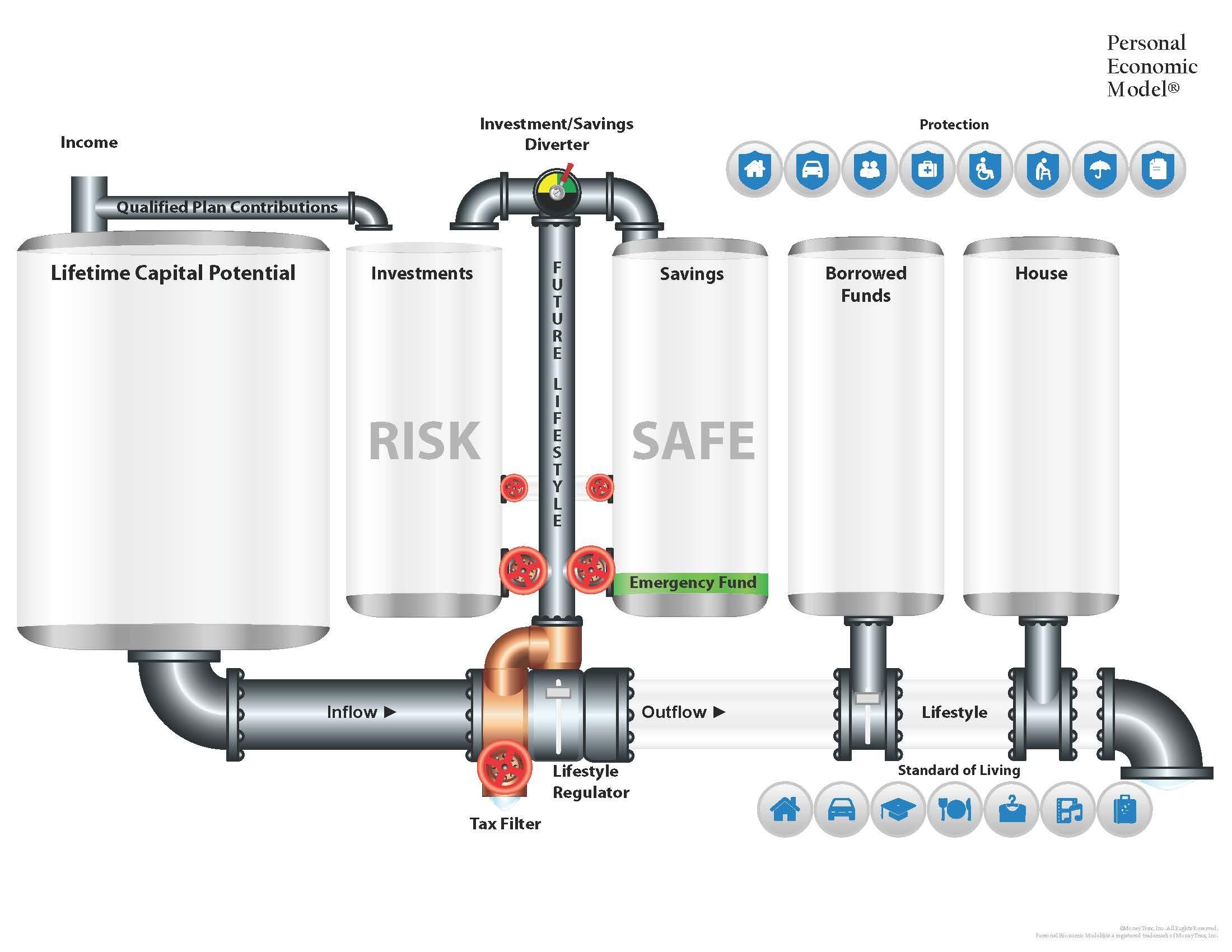

One of the best features of this course is the interactive visual model that Mr. Blanton has created for this course which allows the student to observe what actually happens to their money. This visual is called the Personal Economic Model (PEM). It shows the students exactly what happens to their money, depending on the choices they make. There are investments and savings that may defer taxes, but all money is taxed at some point. (Another belief dispelled is that there is no such thing as tax free earnings.) The visual model includes several tanks that represent money earned, money spent, money invested, and money saved. When students fully understand the financial lessons taught in this class they will be well prepared for life after high school. There is both a biblical and a secular version available. The price is amazing considering the students will have access to many tools and calculators that cost financial advisors a lot more. There are 15 core units, 64 individual lessons, 30 financial calculators, and hours of video instruction.

Students who have completed the 10th grade with a 3.0 GPA can take this class online with Bryan College, for college credit. If you live outside of Tennessee, a $200 scholarship is available, making the three hour class only $300. For Tennessee students, the DE grant will pay for the class if it’s one of the first two classes taken by the student. After the DE grant is used, a $200 scholarship will be offered to Tennessee students as well. The cost of materials is only $75. If you would like to have your student apply to Bryan College as a DE student, use the code bryanhss to waive the application fee.

Students who have completed the 10th grade with a 3.0 GPA can take this class online with Bryan College, for college credit. If you live outside of Tennessee, a $200 scholarship is available, making the three hour class only $300. For Tennessee students, the DE grant will pay for the class if it’s one of the first two classes taken by the student. After the DE grant is used, a $200 scholarship will be offered to Tennessee students as well. The cost of materials is only $75. If you would like to have your student apply to Bryan College as a DE student, use the code bryanhss to waive the application fee.

Students who want to take the class without college credit, or who do not yet qualify for dual enrollment, may take the class at home with a substantial savings. The course is priced at $199 and that includes the materials fee, but if you use this introductory offer code, Intro50, you can save $50 making this course only $149. Parents will appreciate how little work they will have to do with this course.

Take a look at the PEM website. There are a couple of videos worth watching. If you have any questions, let me know and I can put you in touch with Don Blanton, the founder of PEM Life. If what we believe about money isn’t true, the sooner we find out, the better.